Gemini said

Markets don’t break portfolios; emotional reactions do. Build a resilient structure with non-correlated assets—like bonds and real assets—to act as an anchor. Rebalance regularly to sell high and keep "dry powder" ready for when assets go on sale.

Much like building wealth, what is planted, nurtured, and preserved today determines what can be passed on tomorrow. The choices we make, and how we structure them, shape what remains for the next generation.

Beneficiary designations, dependent status, and rollover eligibility can mean the difference between continued tax efficiency and immediate tax erosion. Structure is what decides the result.

Beneficiary designations, dependent status, and rollover eligibility can mean the difference between continued tax efficiency and immediate tax erosion. Structure is what decides the result.

Gemini said

Markets don’t break portfolios; emotional reactions do. Build a resilient structure with non-correlated assets—like bonds and real assets—to act as an anchor. Rebalance regularly to sell high and keep "dry powder" ready for when assets go on sale.

Much like building wealth, what is planted, nurtured, and preserved today determines what can be passed on tomorrow. The choices we make, and how we structure them, shape what remains for the next generation.

Markets are unpredictable, but investor behavior doesn’t have to be. Diversification creates a framework that allows investors to navigate volatility, remain invested through downturns, and benefit from the long-term growth historically demonstrated by the S&P 500.

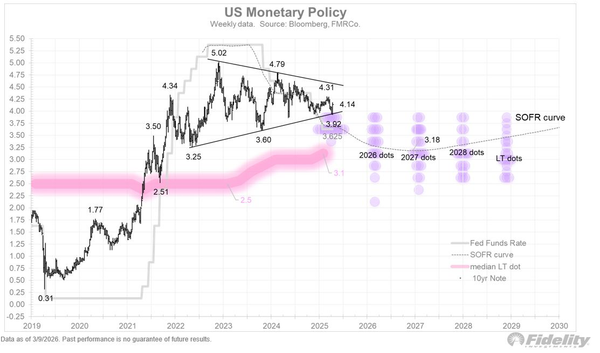

While the U.S. economy has become less sensitive to oil shocks compared to the 1970s, inflation remains persistent enough to keep central banks cautious. The Federal Reserve is not operating in a vacuum, it is responding to a system where inflation has proven more resilient than expected.

Leaders who view contingency planning as a living discipline regularly reassess risk, adjust strategies, and ask the critical question: “What happens if this assumption changes?”

Don’t think that 50 percent pension splitting is enough to fully split retirement income for you and your spouse. Is your employment and future retirement income expected to be significantly higher than your spouse’s? Or vice-versa? That’s when contributions to a Spousal RRSP could be a good idea.

Whether whispered in kitchen conversations, splashed across social media, or cited by worried friends, this “magic number” has become something of a myth.