🧾 Hidden Fees: What’s Actually Behind Your Merchant Statement?

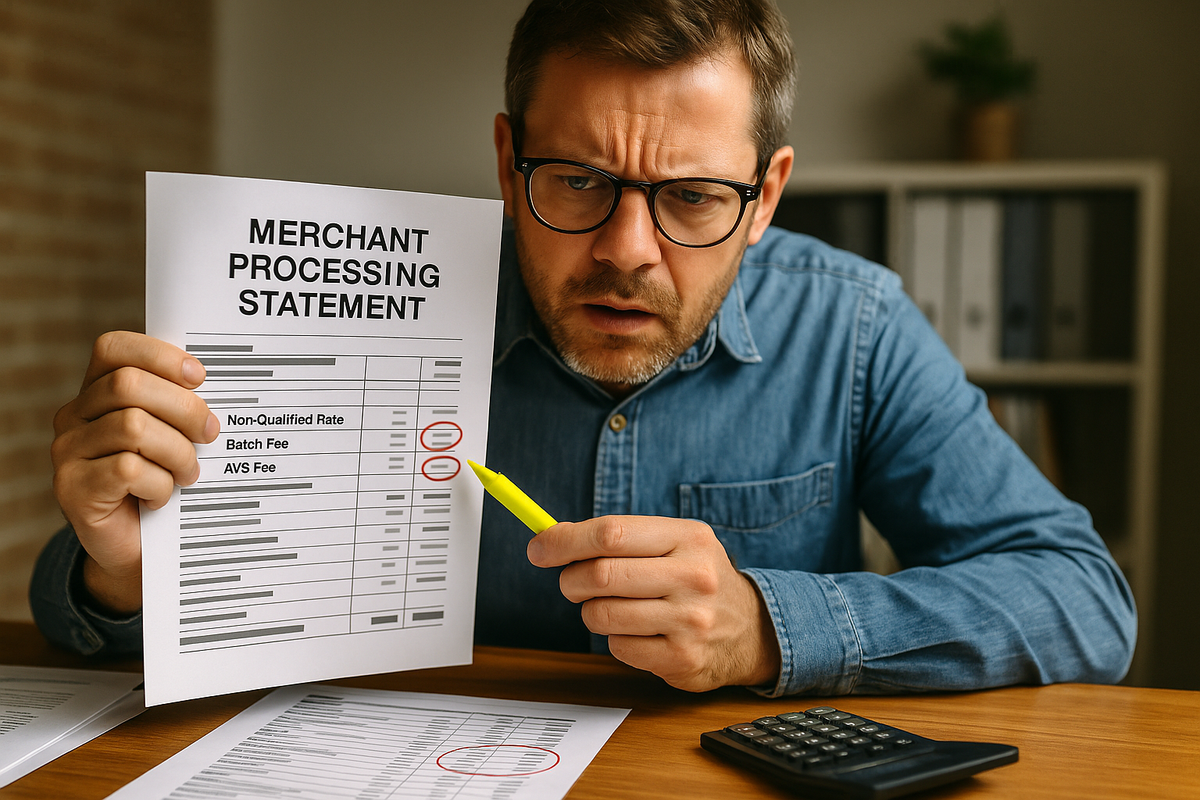

That confusing merchant processing statement? It might be costing you more than you think. Here’s a breakdown of the hidden fees — and how to fight back.

That confusing merchant processing statement? It might be costing you more than you think. Here’s a breakdown of the hidden fees — and how to fight back.