Understanding the Impact of Total Asbestos Exclusion on Business Insurance Policies

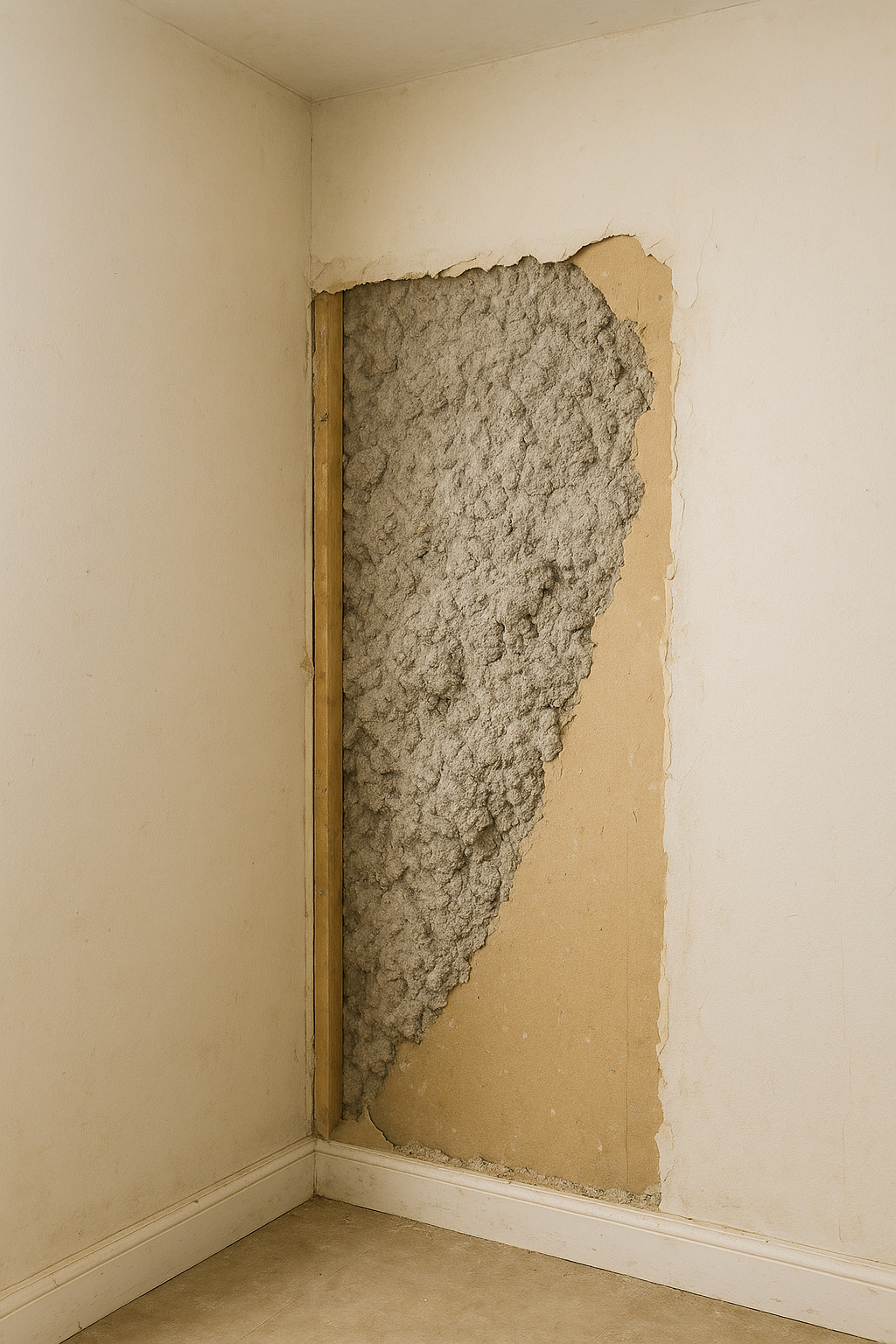

Asbestos exposure can result in severe long-term health issues like mesothelioma, lung cancer, and asbestosis. Claims related to asbestos have historically resulted in massive legal and settlement costs for insurers. Let's talk about it.