Environment and Climate Change Canada (ECCC) has issued an important safety warning for mechanical contractors, HVAC technicians, and refrigerant service providers across Canada. Counterfeit refrigerant cylinders falsely labelled as R-410A have been identified in circulation. Let's talk about it.

I find myself thinking about Abbotsford Connect, our new monthly gathering built for business leaders, entrepreneurs, and community builders. In many ways, the spirit of Christmas and the mission of Abbotsford Connect are beautifully aligned: we gain the most during the experience of giving.

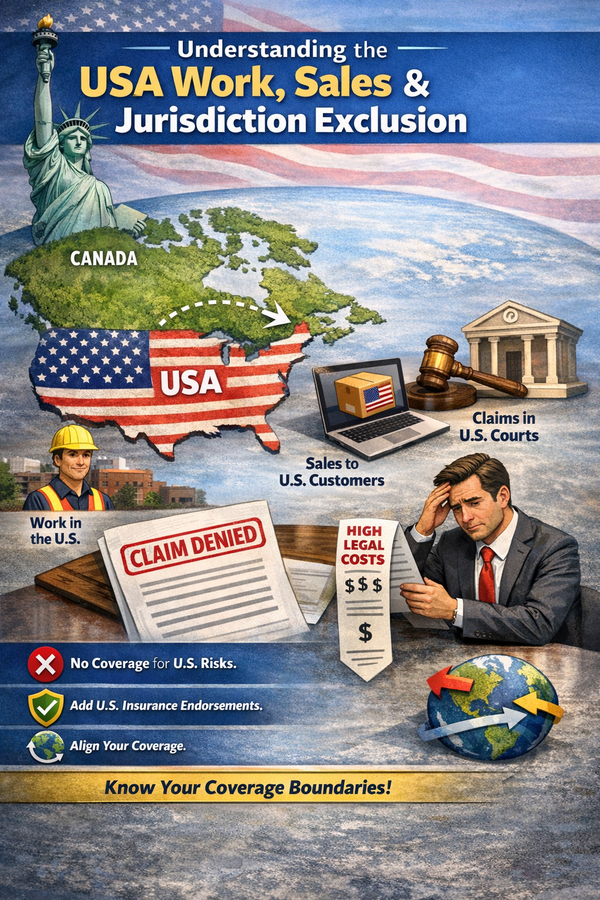

One of the most misunderstood policy provisions in commercial insurance is the USA Work, Sales & Jurisdiction Exclusion. It’s often buried in policy wording, rarely discussed when placing coverage. Let's talk about it.

One of the most misunderstood policy provisions in commercial insurance is the USA Work, Sales & Jurisdiction Exclusion. It’s often buried in policy wording, rarely discussed when placing coverage. Let's talk about it.

Environment and Climate Change Canada (ECCC) has issued an important safety warning for mechanical contractors, HVAC technicians, and refrigerant service providers across Canada. Counterfeit refrigerant cylinders falsely labelled as R-410A have been identified in circulation. Let's talk about it.

I find myself thinking about Abbotsford Connect, our new monthly gathering built for business leaders, entrepreneurs, and community builders. In many ways, the spirit of Christmas and the mission of Abbotsford Connect are beautifully aligned: we gain the most during the experience of giving.

When I first stepped into Langley’s business networking community, I expected what most professionals expect: connections, referrals, and opportunities to grow my business. What I didn’t expect was how profoundly it would reshape my life. Let's talk about it.

My vision is simple: connect people who care about Abbotsford in Abbotsford, while shining a spotlight on the incredible restaurants that make our city such a vibrant place to live and work. First event is January 13, 2026. Are you coming?

45% of BC restaurants are struggling to stay afloat. For many beloved neighbourhood eateries, the difference between surviving and closing their doors for good comes down to one thing—community support. Let's talk about it.

Faulty workmanship coverage protects contractors from the additional costs required to repair or replace damage that arises directly from their own work when that work doesn’t meet the required standards or specifications. Let's talk about it.

What surprises many organizations is that snow removal is often excluded from standard insurance policies, and adding it back in can dramatically raise premiums and possibly make them uninsurable.