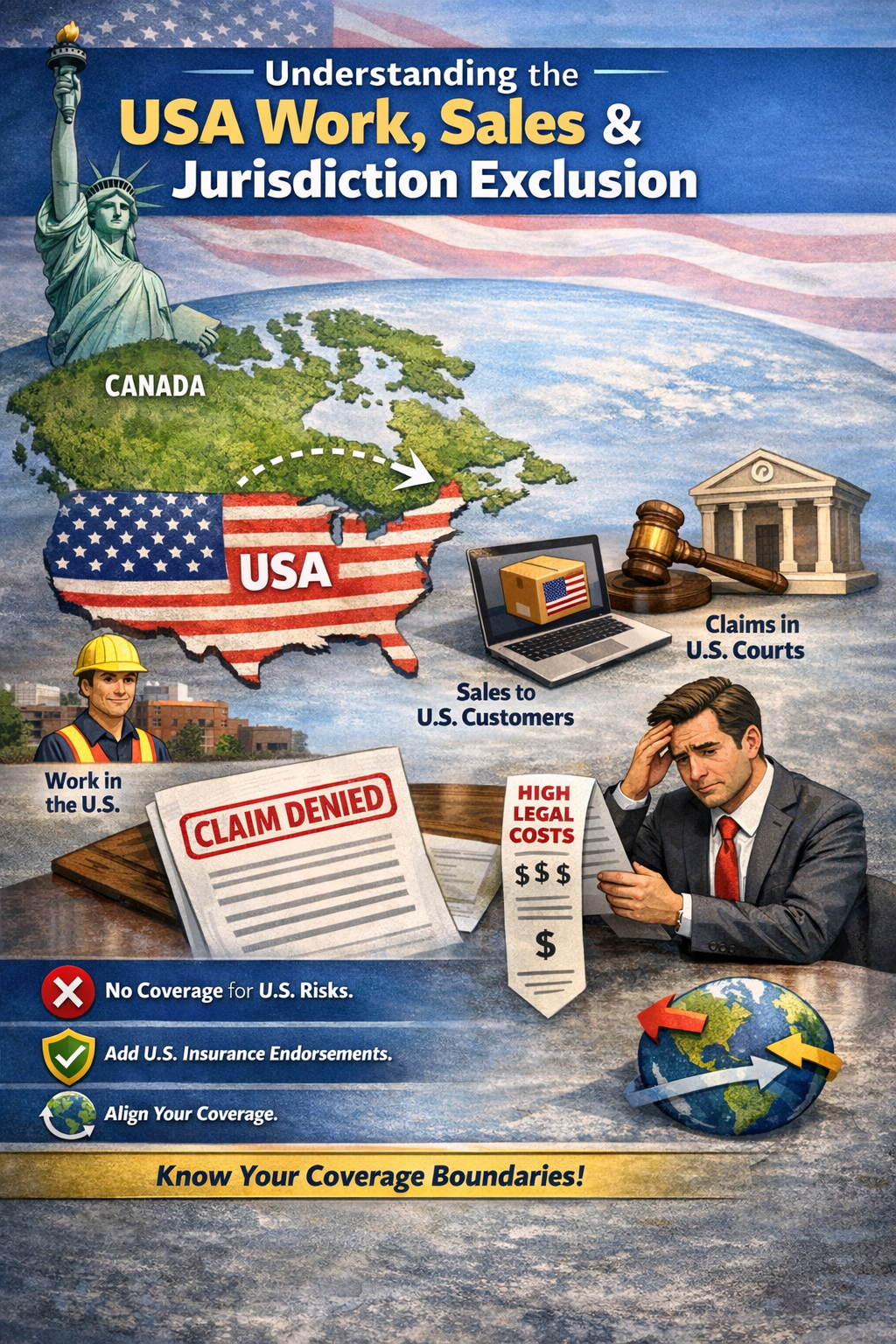

The USA Work, Sales, & Jurisdiction Exclusion: What Business Owners Need to Know

One of the most misunderstood policy provisions in commercial insurance is the USA Work, Sales & Jurisdiction Exclusion. It’s often buried in policy wording, rarely discussed when placing coverage. Let's talk about it.